- The Trump-Xi summit points to a stabilisation in the US-China bilateral relationship and suggests near-term tensions are less likely to escalate further. With potentially three more meetings between Trump and Xi this year, the commitment towards ongoing high-level engagements should help lower geopolitical tail risks on this front. Since the summit, we have seen several positive developments across trade, investment, and technology export controls.

- The CNY is likely to be a clear beneficiary of the summit. We expect the CNY to continue appreciating against the USD over the next 12 months, supported by easing tensions between Washington and Beijing. The improved bilateral relations could encourage international investors to increase exposure to Chinese financial markets as they diversify portfolios amid ongoing US policy uncertainty.

- We remain constructive on both the US and Chinese equities, supported by recent positive developments pointing towards the potential for a more durable truce. In particular, Chinese equities are favourably positioned as global bond yields rise to new highs amid inflation concerns, given China’s diversified energy mix across coal and renewables.

The Trump-Xi Summit points to stabilisation in the US-China relationship

After the US-China summit, both the US and China proposed to establish “a constructive and strategically stable China–US relationship”. This framework highlights four aspects, namely: (i) positive stability focusing on cooperation; (ii) constructive stability characterised by managed competition; (iii) manageable stability based on controlled differences; and (iv) durable stability oriented toward long-term peace. The new positioning is intended to serve as a strategic guidance for US-China relations over the next three years and beyond.

From a trade and investment perspective, there have been several commitments and developments. We believe a major positive outcome relates to the announcement of the establishment of the Board of Trade and the Board of Investment to explore potential tariff reductions and investment in non-sensitive areas, signalling further ongoing high-level communication and commitment towards stabilisation.

On export control and technology, according to media reports, the US Department of Commerce has cleared the sales of the H200 artificial intelligence (AI) chips to 10 Chinese companies, allowing each of them to purchase up to 75,000 H200 chips. That said, China has not officially approved these purchases at the time of writing.

On trade, China announced to purchase 200 Boeing aircrafts, and to renew import licenses for US beef. It is expected that purchases from China could be expanded to US oil and agricultural products, such as, soybeans.

On tariffs, US Treasury Secretary Scott Bessent highlighted that both countries are looking into potential tariff reductions starting with non-sensitive trade worth about USD30bn. Both countries have agreed to establish “the Board of Trade” to explore this issue.

Overall, while the US-China Presidential Summit is unlikely to resolve all disputes and concerns, given the structural disagreements between the US and China on several issues (such as technology export restrictions), we believe the Summit suggests a lower chance of near-term escalation in tensions. Also, the commitment towards ongoing high-level communication and interaction would help minimise chances of de-coupling between US and China. There are potentially three more times that President Trump and President Xi could meet this year, such as: (i) the potential US State visit in September as President Trump invited President Xi to the White House; (ii) APEC Economic Leaders’ Meeting in Shenzhen, China in November; and (iii) G20 Summit in Miami, US in December.

Firmer CNY likely after the summit

The CNY is likely to be a clear beneficiary of the summit. Though the discussions may not have delivered any major breakthroughs, the event appears to have helped stabilise relations between the US and China.

As discussed above, the warmer tone between President Xi and President Trump, the potential for modest deals to purchase US agricultural products and aircraft, fresh talks to lower tariffs on around USD30bn of trade in non-critical goods and discussions to establish a “board of investment” to ease Chinese investment into the US outside sensitive sectors of the US economy signal Washington and Beijing’s desire to put the two countries’ relationship on a firmer footing after last year’s US-led trade war.

A common aim to reopen the Strait of Hormuz to end the energy shock from the US-Iran war also appears likely to keep relations more stable this year despite differences over other geopolitical issues.

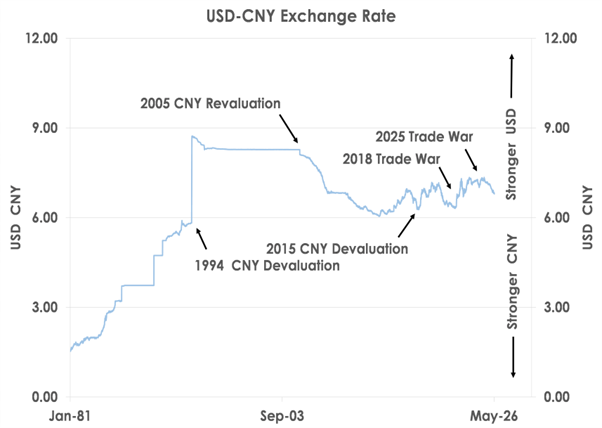

Exhibit 1: USD-CNY Exchange Rate

Source: Bank of Singapore, Bloomberg

We thus expect the CNY will continue to rally against the USD over the next 12 months with the summit now out of the way.

Currently, the currency is trading near 3-year highs of 6.82 against the greenback as the CNY benefits from China’s huge annual trade surplus exceeding USD1tn.

The CNY has been strengthening steadily since hitting a 17-year low of 7.35 against the USD in April last year after President Trump announced his massive tariff increases.

By stabilising relations between the two nations, the summit has reduced the risk of further trade wars during the rest of the Trump administration.

Similarly, easing tensions between Washington and Beijing are likely to spur international investors to increase their exposure towards China’s financial markets. In turn, a stronger CNY is set to keep the USD globally on a multi-year downtrend as investors continue to diversify their portfolios in the face of the Trump administration’s policy shocks.

We thus think further gradual strengthening of the CNY is likely and these developments reinforce our long-term bearish view on the USD globally.

Moderately Overweight on Equities

We recently calibrated our exposures in equities by upgrading US equities from Neutral to Overweight to address upside risk and resilient fundamentals of the AI theme, downgrading Europe equities from Neutral to Underweight given the bloc’s vulnerabilities to energy market uncertainties, while maintaining our Neutral positions in Japan and Asia ex-Japan.

Within Asia ex-Japan, we continue to favour Hong Kong, China and Singapore equity markets. In particular, we believe a combination of compelling valuations, improving earnings revisions, strong Southbound flows, and a more durable trade truce will be supportive factors for Hong Kong and China equities.

Chinese offshore equities (i.e. MSCI China Index) returned on average 1-5% in the 1-3 months after President Trump and President Xi’s face-to-face meetings since 2017, suggesting that investors have tended to perceive high-level Presidential in-person meetings as market-stabilising events. On the other hand, the onshore A-share equities market is more sensitive to domestic issues and policies.

With the stabilisation in US-China relations, this could enable investors to focus back on fundamentals. From a macro perspective, the market has continued focusing on risks from a potential prolonged Strait of Hormuz disruption and therefore the impact on oil prices and inflation. Global bond yields have inched into new highs, triggering equity market volatility. We believe Chinese equities are well positioned given China has a relatively low reliance on oil via the Strait of Hormuz and a diversified energy mix in coal and renewables. The onshore A-share market is also well positioned as it has one of the lowest correlation with US equities among Asian equity markets. We reiterate our relative preference for the onshore A-share market which could benefit from the focus on “AI+” and technology innovation initiatives, given more than two-thirds of the market cap is from industrials, IT and related services.

Despite the clearance of the sale of H200 AI chips, we believe that China’s semiconductor localisation drive, which is part of the “AI+” and technology innovation initiatives, will stay intact. First, state-supported and affiliated data centers are likely to continue to purchase domestic AI chips. Second, the reported 750,000 H200 chips sales allowance is unlikely to fully meet the demand from the robust CAPEX plans of domestic cloud service providers as well as internet and platform companies. Third, domestic chips are likely to match the performance of H200 next year.

Leading internet and platform companies (which are also index heavy companies) that have reported 1Q26 results so far have reaffirmed that food delivery and quick commerce losses have narrowed substantially. We believe it could help alleviate market concerns of further earnings drag. They also demonstrated a strong commitment to AI infrastructure investment and CAPEX growth, which should have a positive spillover impact to the AI supply chain.

From a sector perspective, Energy, Industrials and Materials offer favourable earnings growth. We reiterate a barbell strategy with quality yield plays to cushion market volatility and to benefit from policymakers’ rising focus on shareholders’ return. We believe structural themes will offer upside optionality, including: (i) AI proxies; and (ii) policy beneficiaries in technology innovation, domestic consumption and anti-involution.

This article was first published by Bank of Singapore on 19 May 2026. The Opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of OCBC Private Bank or its affiliates.OCBC Private Bank provides a suite of products for wealth creation, preservation and transmission including holistic wealth management services, independent research, customized solutions for all investor preferences, and genuine open architecture, with expertise in Indonesia and Asia Pacific markets. OCBC Private Bank is a part of OCBC Group.